ลองดูแบบนี้ละกัน

หลังๆ ผมรู้สึกผมซื้อขายมั่วซั่วไปหน่อย จนทำให้ Performance ผมแย่ลงโดยไม่จำเป็น คืออยู่เฉยๆ ตั้งแต่ต้นปี พอร์ตน่าจะกำไรดีกว่านี้หลาย % อะ

พอคิดดูแล้วสาเหตุหลักๆ มันมาจากการที่ผมควบคุมอารมณ์ตัวเองที่เหวี่ยงไปตามราคาไม่ได้ แล้วก็เทรด พอราคาขึ้นก็ Bullish กลัวตกรถ ราคาลงก็กลัว performance จะแย่กว่านี้จนแพ้ตลาด (ซึ่งจริงๆ แล้วเราไม่ควรสนใจตลาดในระยะสั้นนะ) มันมั่วซั่วไปหมด

จริงๆ ผมเองก็มีกฎการซื้อขายให้ตัวเองนะ เช่น 1) ถ้าจะซื้อขายต้องทำ Valuation ดีๆ ก่อน 2) ต้องจดโน๊ทให้ชัดเจน 3) ซื้อขายแค่อาทิตย์ละวัน และอื่นๆ แต่พอเวลาผ่านไป แม่งทำไม่ค่อยได้ ==”

ถ้าผมอยากรักษากฎให้ดีกว่านี้ มันมีวิธีนึงที่เพิ่ม accountability ให้กับตัวเอง นั่นก็คือการบอกคนอื่นไปเลย ว่าเราถืออะไรบ้าง แล้วทำไมเราถึงซื้อ/ขายหุ้นแต่ละตัว ในพอร์ตเรา

จริงๆ ก็คิดมานานแล้วว่าจะทำ แต่ไม่กล้าทำซักทีเพราะมันมีข้อเสียเยอะอยู่ ที่คิดออกตอนนี้เลยก็ 1) ถ้าพอร์ตกาก ก็คงขายหน้าน่าดู 2) ถ้าเปลี่ยนใจไปมา ก็ดูโง่ๆ เหมือนกัน 3) ถ้ากำไรเยอะอาจโดนเพ่งเล็ง จาก….

แต่ ณ จุดนี้ผมว่าผมว่าข้อดีน่าจะมีมากกว่าข้อเสียละ ผมเชื่อว่าถ้าผมเขียนอธิบายให้คนรับรู้ก่อนเทรด ผมจะไม่เทรดมั่วซั่วขนาดนี้ และมันน่าจะทำให้ผมทำกำไรได้ดีขึ้น นอกจากนี้ผมจะได้รักษา Trading Rule ของผมได้ดีขึ้นด้วย เพราะเรารู้ว่าอินเตอร์เน็ตกับกำลัง

ก็เลยว่า เอาวะลองดูละกัน.. เพื่อตัวเองล้วนๆ เริ่มจาก Substack ในนี้ก่อนเลย คนติดตามไม่ได้เยอะมาก แต่ก็เยอะพอให้รักษา accountability ของตัวเอง

Checklist before buying or selling

ก่อนอื่น ขอแชร์ checklist ของผม (เพิ่งอัพเดตมาสดๆ ร้อนๆ) นี่คือกฎที่ผมต้องทำให้ได้ ก่อนที่จะซื้อขายหุ้นตัวใดตัวหนึ่ง

หลายข้อมันอาจจะทำให้ผมเสียโอกาสบ้าง แต่น่าจะทำให้ผมไม่ทำอะไรโง่ๆ ด้วย

Before Opening Position:

Must have done a write up before. » ไว้ว่างๆ เวลาอ่านบริษัทใหม่จะมาเขียนในนี้ว่าบริษัทนี้ทำอะไร

Has some type of Valuation Model before » คร่าวๆ ว่าตลาดคาดหวังอะไร แค่ไหน

Trading Rules:

Always write in the trade journal when making the trades - including valuation part » เขียนสรุปสั้นๆ อีกรอบก่อนซื้อขาย พร้อม valuation อีกรอบ

Always cross-check with a trusted person (exclude the introducer) » ยังไม่เคยลอง ว่าจะลองดู

Always complete the checklist for emotion before executing. » ผมมีเช็คลิสต์ทางอารมณ์อีกอัน แต่ถ้าโพสต์ในเน็ตแบบนี้แล้ว ความสำคัญของ emotion checklist ดังกล่าวน่าจะลดลง

No buying or selling 1 day after earnings calls. It messes up the habit. » บางทีทำแล้วเวิร์ค แต่ไม่เวิร์คก็มีอะ

Limits:

Limit buy to 10 stocks a year. (4 Stocks left this year for Aug 2025)

Max of 3 Tickers to buy or sell per week.

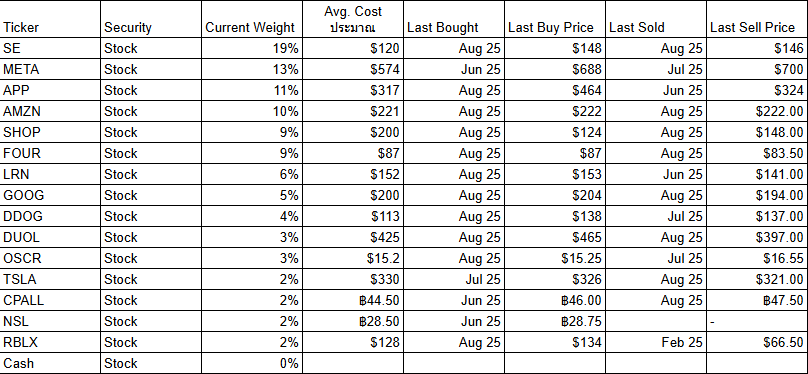

My Portfolio

จริงๆ ผมอยากใส่ตัวเลขต้นทุนเฉลี่ยด้วย ผมว่ามันโปร่งใสดี แต่พอลองทำดูแล้วมันมั่วไปหมดเพราะผมมีหลายพอร์ต บางอันเป็น DR ไรงี้ ครั้งนี้เลยขอเป็นแค่สัดส่วน และ Last Buy / Last Sold และทุนโดยประมาณ แล้วต่อไปนี้ผมจะรายงานการซื้อขายของผมทั้งหมด

เสียวมากเลย บ่องตง เพราะบางอันขายโง่ซื้อโง่มากเลย แต่ก็ตามนี้แหละ Here we Go!

YTD รวมทุกพอร์ตน่าจะบวกประมาณ +/- 25% ได้ครับ ยังไม่ได้เคาะดีๆ

diclaimer: นี่ไม่ใช่คำแนะนำการลงทุนนะครับ ทุกการลงทุนมีความเสี่ยง ศึกษาและตัดสินใจด้วยตัวเองก่อนลงทุนเสมอ

ถ้าลองดูจะเห็นเลยว่า ผมจิ้มซื้อๆ ขายๆ บ่อย เพราะไม่ค่อยมั่นใจตอนราคาหุ้นแต่ละตัวมันขึ้นมา ต้นทุนก็สูงตาม แล้วก็มีไป FOMO RBLX กับ DUOL มาด้วย! (บางตัว FOMO ตามก็ได้ตังค์นะ แต่คือแบบนี้มันไม่เวิร์ค) ไอพวกที่ FOMO ตามเนี่ยทำเสียเซลฟ์พอสมควร ไอตัวที่ขายดันขึ้นด้วยแบบ SE กับ Affirm

เข้าใจรึยังว่าทำไมถึงต้องอัพเดตพอร์ตแบบนี้! T.T

ผมว่าเดี๋ยวผมอาจจะขายหุ้นที่ผมไม่ค่อยมั่นใจออก เพราะผมอยากถือเงินสดไว้บ้าง ไว้เดี๋ยวมาอัพเดตครับ

ปล. ผมว่าจะทำเป็นบริการแบบเก็บตังค์ในอนาคต พร้อมมี Weekly Newsletter และอื่นๆ เป็นธุรกิจเล็กๆ อันนึงครับ จะได้มีแรงกระตุ้นให้ทำได้ต่อเนื่อง เพื่อนคิดว่าไง? แต่ตอนนี้เอาเท่านี้ไปก่อน

ไหนๆ ก็โชว์ Holdings ไปแล้ว ผมขอเอาบันทึกที่ผมเคยเขียนไว้ให้ญาติๆ เมื่อเกือบสองเดือนที่แล้ว ว่าทำไมผมถึงถือแต่ละตัว มาแปะไว้ด้วยเลยละกัน (รวมถึงหุ้นที่ผมขาย 🐷ไปแล้วด้วย)

ลองสังเกตุดูว่าจากตอนนั้นมาตอนนี้ หน้าหุ้นผมก็เปลี่ยนไปเยอะอีกแล้ว แต่ไว้ผมค่อยหาเวลามาคอมเม้นต์อีกที รายละเอียดตามนี้ครับ

June 27, 2025 - 2025 H1 Letter to Cleints

Performance:

YTD performance: About 17% constant currency. (11% with baht strengthening)

Vs QQQ 6%, SPY 4%

Market condition and exposure:

The market movement in the first half of the year has been nothing short of dramatic. The market started the year with full optimism about AI impacts and the new business friendly administration. Then Trump turns the narrative upside down with his Tariffs plan that everyone feared will cause global recession. The stock market reacted by entering a bear market which later turned out to be one of the shortest bear markets in history (1 month!) as the administration sorted out the unrealistic tariff level while the economy seemed to coast through without any problem. GDP growth is fine. Inflation is under control. The market expects the Fed to lower rates. Now, despite conflicts erupting around the world, the narrative swings back to how A.I. will help unlock productivity, reducing the alarming US national debt level.

The optimism is, in my opinion, justified. Every tech leader talked about how it will change the world (probably except those at Apple!). Led by chatGPT, LLM-based A.I diffused at the fastest pace ever. It has proved to be very life-changing. This is an internet-level phenomena.

Turns out Liberation day bear market was the last chance to get into AI beneficiary stocks for the cheap. April 2-9 was the time where everyone, somehow, just forgot how ChatGPT will change the world. If there is a big trend emerging that you believe in, the best time to buy is when the market somehow suddenly forgets about its significance for a few moments.

If there is another chance, I will remind myself that the next best time to invest in AI is when the market briefly forgets about the potential of AI.

If the stock market is a party, this is when music is getting louder and the dance floor has become much more inviting. We see many themed retail stocks shooting through the roof. Those related to AI include chip manufacturers, energy and nuclear (SMR), and relatedly quantum computing. Another theme that drew in the crowd is stablecoin and crypto. Circle 8Xed in a month after its IPO was a good example. SaaS and bigtech also saw multiple expansion. All of these represent attractive girls dancing on the dance floor, while those who already profit from them are becoming more intoxicated. The market P/E Ratio is also quite high which, if history is any guide, means that average returns over the next few years will be worse than average return of the market) [pic]

Also, there are a few signals that I used to time the market top.

1) Equity Risk Premium dipping below 4.0%

2) Howard Mark's Checklist score on a high range

3) Market P/E is at the high end of the historical range.

4) Buffett Buy Back indicator showing no share buyback

5) Fear Greed Index Shows greediness

6) Own Watchlist stocks reaching or exceeding high end of valuation range

Currently a few indicators (2,3,4,6) are flashing yellow. More explanation in this video: 5 สัญญาณเตือนหุ้นแพง ที่ผมใช้ในการ Timing ตลาด

There are still people standing at the sideline of the floor, hesitating to dance at this party. Why?

I believe there are still worries and fears, such as ballooning U.S. deficits, the ongoing tariffs deal which has been extended until 14th July, and wars going around the world. The wound from the previous downturn was also fresh. The Liberation day crash was very recent. And the techstock meltdown was only 3 years ago (I, included, have PTSD on this lol). This is not long enough for a wave of new generations who have never experienced a bubble before to join.

So my guess is, the time is about 10PM and the night is still long. Therefore, my allocation plan is to stay fully invested, for now. Riding the wall of worries.

Even if you dance early, if you refuse to stop, you will end up cleaning up the place! Therefore, I will start to slowly raise cash if the overall market rips higher. The plan is if Nasdaq100 hit >10% YTD performance, I might reduce my holdings by 10%, and reduce further as the market rises.

All that said, timing the stock market is hard, and I will only reduce my holding by no more than 30%. Time in market and stock selection is still more important.

Stock selection style:

Stick to what I understand well and clearly see how it will be in 10 years.

Try to avoid hot stocks that I don’t know well. Upstream A.I. is such an example. The field moves really fast. I would rather focus on finding which companies I follow are a great beneficiary of AI that Wall Street hasn't fully realized yet. Generally catching new trends early and riding along is not really my style.

Look for aligned management. Founder-type preferred.

Don’t buy at a price too high. Only switch when the company in the portfolio is super expensive or misjudged.

Now on to top holding updates.

Top Holdings (approximate allocation):

SE - Sea Limited. (20%+)

Sea Limited can be broken down into two parts: E-commerce (Shopee) and Games (Garena). Some analysts also choose to split lending business out from the E-commerce business but it is fine either way.

For more detail, access more detail in Tab “Write up”: Sea Limited (SE)

E-commerce Thesis:

Massive E-commerce GMV Runway in SEA through 1) e-com penetration 2) spend per user (more products and frequency) Supported by SEA GDP Growth of 4-5% per year. 3) Option to take share in Brazil and other countries. Expect GMV growth >10% for a long time.

Possibility of following Amazon strategy of subscription (Prime).

Possibility to increase take rate through lessen competition and advertising.

A period of intense competition has passed. 1) land grab phase done. 2) winners consolidate 3) higher cost of capital & mindset shift to profit. Network Effects. This allows Shopee to increase take rate. Other players also follow suit.

Threats and risks include New price war from new way to acquire customer and Personal AI acting as a middleman.

Financial Service:

Lots of unbanked population. Digital Native Users, smart phone as first device. Lots of data from Shopee platform

Other good traits.

Founder-led, Best in class team. Nimble. Weathered intense competition. Founder-led. Largest Scale in region.

Increased competition in Indonesia (grab,Tiktok,Tokopedia merging) and Brazil (Mercado Libre).

Games Business

Less Hit-driven than believed through improved Live ops. SE has a core user and expertise in the business. Has lots of data. Large studio has advantage as games require more investment these days. User Acquisition will get harder by the days.

Undemanding valuation 10X EBITDA gives you 12 Billion. Game business returning 10%+ per year should be no problem. Pricing it at 8x EBITDA with minimal D&A means about 10% Cash return each year.

Positive trend: More discretionary spending on games.

Concerns: Competition from Tencent.

Expectation. Expect GMV growth to be around Mid-teens in the next 8-9 years. (Follow Amazon curve in terms of growth and GMV per capita.). Given Net Income as % GMV at 4% yields and IRR of around 15% (2% Cash return included.)

AMZN (< 20%)

Thesis:

Still revenue growth runway in ecommerce, groceries, prime and more.

Lots of room for margin improvement through operating leverage in e-commerce business.

Beneficiary of drones and robots adoption

Room to grow in the ads business into CTV and other sites.

Temu and other Chinese competitors get affected more by tariffs. Reduction in tariff possible

AWS is riding the AI wave but modestly.

Major Risk:

AWS lagging behind in AI. Worse offering and limited nVidia GPU allocation.

Ads and E-commerce somehow slow down faster than believed.

Trade and tariffs problem could arise again anytime.

META (< 20%)

หุ้น META กับแผนที่จะทำให้หุ้นไปถึง $1000 ใน 2 ปี

Thesis:

A.I. reduces cost of content production and sales support which leads to more budget towards digital ads spending.

A.I. continues to improve recommendations, both in ads and content.

More surface area to ads. Whatsapp mostly.

Risks:

AI takes time share from entertainment (not yet, for now)

High Capital investment projects yield bad returns. Could be due to bad execution such as failing to gain chatbot market share (Meta is currently going through AI heads shake up), or just bad decisions, such as being too early on Metaverse or wearables.

High Capex means low free cash flow.

Regulation. Most concern is in the EU.

Valuation is getting more demanding. Market is believing that its Capex spend will be put to good use. If that turns out not to be the case, Zuck will be questioned by the market again. But I’m optimistic about the ads part.

SHOP (< 10%)

Shopify will continue to leverage its scale and excellence to out-dev its competition, while also improving its profit margin.

Good traits: Very sticky (almost ERP-like). Lead in technology. Great founder. Lots of optionality and revenue expansion (capital, audience, for example). A.I. beneficiary.

Major Risks:

Valuation: Rather demanding valuation. Slowing customer addition to MSD%. Broad e-commerce slowdown.

Tariff impact popping back up. Inflation as well (but no need to fear it unnecessarily)

DDOG (< 10%)

One of the cheaper saas names that can still grow along with cloud and AI usage. Their services are becoming more mission critical and proved to provide real value to customers who decided to pay more for value (lower TCO, lower incident cost).

I think they will gain R&D leverage similar to Shopify and outcompete their competitor.

Growth is quite obvious and is not seat-based.

Founder-led as well.

Risk:

Pricing pressure from competition as A.I. allows competition to catch up on its feature fast.

Gross margin compression as more AI is diffused into its product use cases.

FOUR (< 10%)

More info on the stock:

The company seems to have a sound strategy of M&A with a proven track record, yet the market is still in the wait and see mode. Good upside if they execute.

Reasonable valuation. Room for upside at MSD EV/FCF in 2028.

Founder-like CEO. Great capital allocation. Overlooked.

Risks: Falling behind technologically vs more high-tech competitor, Stable coin eating up interchange fee and margin. Execution risk. High Debt

APP (< 10%)

Thesis: Applovin continues to dominate Mobile App Install market, with room to expand to adjacent In-App-Purchase market.

The stock is rather very expensive at 60P/E and 24x Forward EV/S multiple. Even though it is still growing fast, we are betting on continuous improvement in its ads recommendation system and market dominance.

The upside will be on its ability to expand to e-commerce and the AI flywheel thesis similar to META’s. The management team is phenomenal and aligned.

This stock has a high downside and if it goes higher, I will consider selling it may be at $400+

More Speculative bets:

AFRM (< 5%)

This is one of the more risky bets. It’s somewhat a bet that the party is still going. Its performance also depends on good macro numbers (GDP, Inflation).

However, there is room for upside for good execution. Revenue base is still quite small vs all e-commerce. Tech is rather proven. Cost under control. Partnership is good.

The coming of stable coin might help reducing reliance on credit card network.

TSLA (< 5%)

I bought TSLA during Robotaxi’s launch period out of FOMO. After thinking through it, I felt stupid. Tesla still has a lot to prove on the technology front (especially safety). As well as a lot of operation side of work to do.

Elon always puts up a surprise though. If they somehow expand fast, the stock might be ok. But if there is no sign, I will reduce it soon.

More rumination here EP.44 Tesla จะ Disrupt Uber ไหม?

OSCR (< 5%)

Cheap stock but with policy concern. I’m still doing more homework on this.

More info here: EP.43 หุ้น Oscar Health + Stable Coin vs VISA + Meta ตามหลัง AI!?

Stocks I sold

RCL - I liked the stock and continue to like it today. Clear long-term trend. Fear of recession and news about taxing the ships during the start of the administration to gain more revenue for the country caused me to sell RCL at about $240. The stock is now (check ticker..) $306!! Totally missed the ride back to the high. T.T. However, at this price, I would not get in as the upside is rather limited (require full valuation - 20x, 5% pricing growth, full capacity production, and no recession in the next 8 years to get 12% IRR). Looking back, Getting off too early due to recession and policy scare was a big mistake as I already have a source that shows cruise pricing almost daily, I could have just waited for this signal to ring before selling. Turns out the economy is great and people are still cruising more than ever. Trust the raw data, not the narrative.

LRN - I sold Stride off around $140-150. The valuation is still not too demanding (teens multiple) but the recent news about the school district dropping stride due to student’s performance (again!) spooked me. I’m worried about limited career learning growth (penetrating to all students). I am also worried how AI will change the homeschooling landscape, it might take time but it will come all at once. So I bagged the gain and see whether the company utilize AI better than competitors (startups and public school).

TCOM - I never have much conviction in TCOM except from its product, Trip.com. It’s hard to give the right multiple in the China’s business, which is still worth a lot to TCOM total market cap. Apart from the product, the valuation is undemanding and it is riding secular market growth.

AI chatbot disintermediation and Chinese competition (JD joined the fight) added a bit more uncertainty so I decide to move to other names. If it becomes cheaper, may be $45-50, I will consider rejoin.

CRWD - Best quality cybersec name. Sold too early due to valuation (20x+ p/s), again! I’m not very good at holding expensive names. Too much focus on valuation. My decision might proven to be right over the next few years though. We shall see and learn.

FRFHF - Bought as a cash replacement as it has room to compound rather safely. Since then it has been performing much better than I thought. P/B of the stock is now at 1.7x, a historically high range, even higher than Berkshire’s P/B. Clearly, judging the company using a single ratio is never productive. According to unrivaled investing, the company’s profit is positioned to grow MDD%, which deserves a higher book. I wouldn’t join in now though (but I said it since 1.3x).